When it comes to life insurance we naturally first look to cover the breadwinners. Often overlooked are stay-at-home parents.

Although the number of stay-at-home parents in two-parent homes has been in sharp decline since the 70’s, according to Statistics Canada 18% of households choose to have one parent stay-at-home. In another study it showed that while 70% of working moms said their decision was based on what made the most financial sense for their family, 66% of stay-at-home moms put the well-being of their children as the number one reason for their choice.

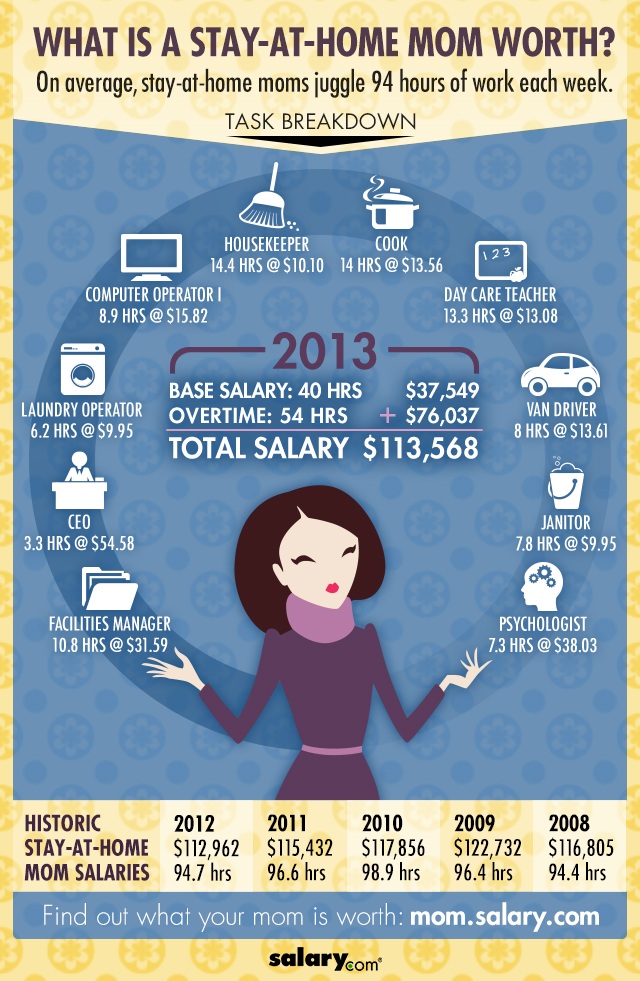

Whatever the motivation, the decision to stay at home often means leaving behind employer-sponsored life, disability, health & dental, and other insurance. Moreover, studies like the one at Salary.com indicate that being a stay-at-home mom doesn’t necessarily mean that their value to the home is any less. In fact, it’s quite the opposite. The total salary for an average working mom including work at home was $67,436. Contrast that to a stay-at-home mom who’s total worth in salary is estimated at $113,568.

That being said, it is vital for stay-at-home parents to retain life and other types of insurance that reflect the true value of their contribution to the household. Here’s a checklist of things you can use to ensure that your stay-at-home spouse is properly covered:

1. Child care. Your children may require daycare, which for a preschooler can cost $8,000 or more per year. A full-time nanny will cost $40,000 a year or more.

2. Housework. A weekly visit from a housekeeper can easily add up to a bill close to $5,000 per year.

3. Income replacement. As the surviving spouse you will have to take on additional responsibilities and as a result may not devote as much time to work resulting in a potential decline in income.

4. Household maintenance. The hourly cost for a repair person can be costly, and even more so for a professional tradesman.

5. Immediate needs. These might include estate settlement costs, tax liabilities, and outstanding debts, all of which could easily drain cash resources.

Protecting your family and ensuring you can meet your financial goals means we should also consider the value of these unpaid services when determining your insurance needs. All of this can be done with the assistance of a trusted financial advisor.

If you have any questions about this article or would like the assistance of one of our licensed professionals, please call us at 1.416.759.5453 or email us at info@lilandinsurance.com.